As a Chartered Accountant, I spend my days staring at spreadsheets so you don’t have to. But today, I’m putting down the calculator and picking up the digital pen. Why? Because the most common question I get at dinner parties (yes, I’m that fun) is: “Should I stay a Sole Trader or go Limited?”

With the 2025/26 tax year wrapping up and the 2026/27 year starting on 6 April, the math has shifted. The government has tweaked the dials on National Insurance and Dividend taxes, making the “winner” less obvious than it used to be.

Let’s dive into the ultimate showdown for consultants.

The Contenders: Sole Trader vs. Limited Company

Before we look at the numbers, let’s meet our competitors:

-

The Sole Trader: Simple, low admin, and you are the business. You pay Income Tax and National Insurance (NICs) on all your profits.

-

The Limited Company: A separate legal “person.” You pay Corporation Tax on profits, then pay yourself via a mix of low salary and dividends. It’s fancier, but it comes with more paperwork.

Key Tax Rates for 2026/27

To keep things simple, here are the main rates we’re playing with for the upcoming year (based on HMRC guidance):

| Tax Type | Rate/Detail (2026/27) |

| Personal Allowance | £12,570 (Tax-free!) |

| Basic Rate Income Tax | 20% (£12,571 – £50,270) |

| Class 4 NICs (Sole Trader) | 6% on profits up to £50,270 |

| Corporation Tax | 19% (up to £50k) / 25% (over £250k) |

| Dividend Tax (Basic Rate) | 10.75% (Up from 8.75%!) |

| Employer NICs | 15% (on salaries over £5,000) |

Scenario: The “Successful Sarah” Case Study

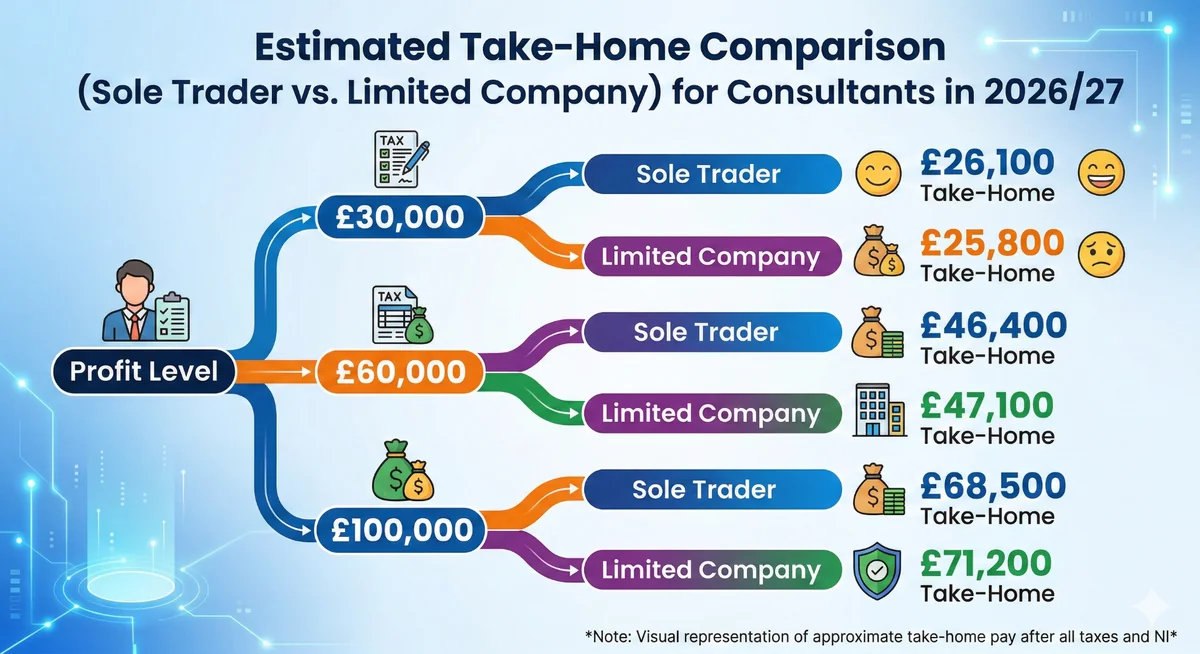

Sarah is a Management Consultant. She expects to make £60,000 in “profit” (income after expenses but before tax). Let’s see how she fares in the 2026/27 tax year.

1. Sarah as a Sole Trader

Sarah pays Income Tax and Class 4 NICs. It’s straightforward, but there’s nowhere to hide from the taxman.

-

Total Tax & NICs: Approx. £13,600

-

Take-Home: Approx. £46,400

2. Sarah as a Limited Company Director

Sarah pays herself a tiny salary (around the NI threshold) and takes the rest as dividends.

-

Corporation Tax (19%): The company pays this first.

-

Dividend Tax (10.75%): Sarah pays this on what’s left.

-

Total Tax: Approx. £12,900

-

Take-Home: Approx. £47,100

The Verdict for Sarah: She saves about £700 by being a Limited Company. Is that enough to cover the extra accountancy fees and the headache of filing Company House returns? For many, the answer is “maybe not.”

The “Tax Efficiency” Heatmap

As your income climbs, the Limited Company usually starts to pull ahead. However, with the dividend tax hike to 10.75% and Employer NI at 15%, the gap is narrowing faster than my waistline after a holiday.

Estimated Take-Home Comparison (2026/27)

Beyond the Numbers: The “Fun” Stuff

Tax isn’t everything (I know, heresy!). Here are three things Sarah needs to consider:

Credibility: Some big corporate clients simply won’t hire you unless you’re “Sarah Consulting Ltd.” It looks more “established.”

Liability: As a Sole Trader, if you accidentally advise a client to buy a lemon of a company, your house is on the line. As a Limited Company, the company is liable.

The “Tax Deferral” Trick: If Sarah doesn’t need all £60k to live on, she can leave the money in the company, pay 19% Corporation Tax, and take the dividends in a future year when she might be in a lower tax bracket. Sole traders can’t do that—they are taxed on every penny the year they earn it.

Which one is right for you?

If you’re making under £40,000, the Sole Trader route is likely your best bet for simplicity. Once you cross the £50,000 mark, it’s time for us to have a “grown-up” chat about incorporating.

Important Links:

Check your current Income Tax rates.

Read up on Running a Limited Company.

Still confused? Don’t worry, that’s why people like me exist!