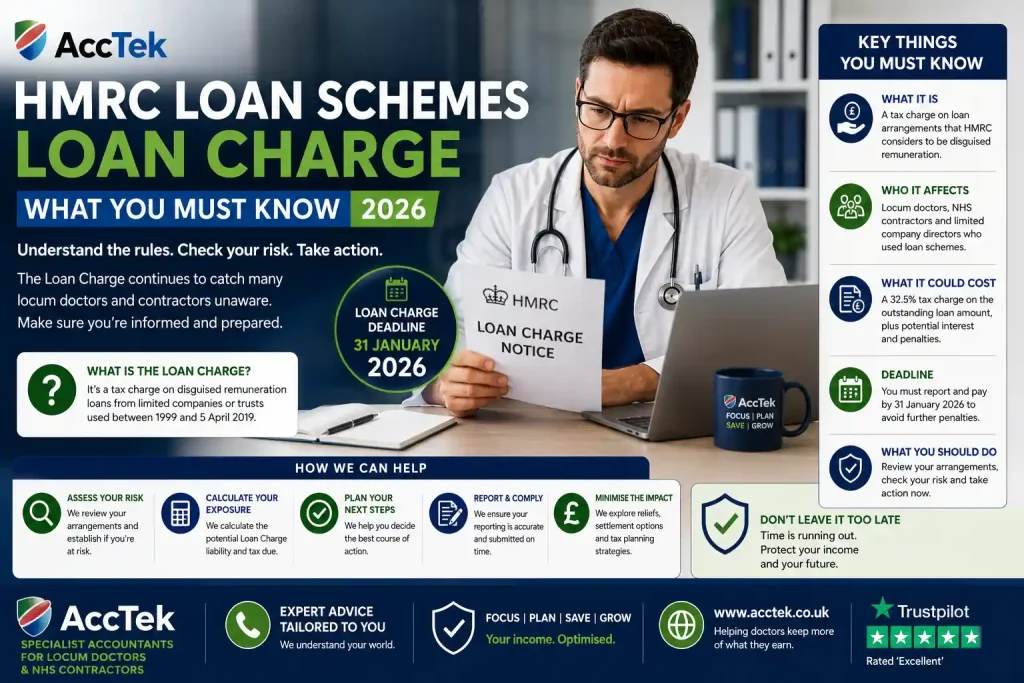

HMRC has refreshed its guidance on tax avoidance loan schemes and the loan charge—a critical reminder that the taxman remains focused on high-risk avoidance arrangements. If you’ve used a loan scheme in the past or are uncertain whether you’re at risk, this updated publication demands immediate attention.

HMRC’s updated overview on loan schemes and the loan charge doesn’t announce a brand-new tax rule—the loan charge itself has been in force since April 2019—but the republication signals renewed enforcement activity and clarified guidance on what HMRC considers a flagged avoidance arrangement.

The loan charge applies to borrowers who participated in tax avoidance loan schemes. In essence, HMRC treats the borrowed funds as income in the tax year the loan scheme comes to an end, or when you leave the arrangement, unless:

The key effective date remains 5 April 2019, when the loan charge legislation took effect. However, HMRC’s refreshed publication confirms they are actively pursuing those who have not yet settled, and penalties remain significant: up to 100% of the unpaid tax for deliberate non-disclosure, or 30% for careless defaults.

The publication reaffirms HMRC’s focus on identifying participants in marketed avoidance schemes, particularly those involved in film partnerships, employment trusts, employer-financed retirement benefit schemes, and other complex loan-based structures marketed between 1999 and 2019.

If you’re an IT contractor or locum doctor earning between £50,000 and £200,000 per annum, you’ve been a prime target for these schemes. The commercial appeal was simple: borrow funds from a scheme promoter, claim the borrowed amount is a non-taxable loan, and retain far more cash than a straightforward employment or self-employment arrangement would allow.

The reality now is stark. HMRC has matched its records against scheme promoter disclosures and is issuing discovery assessments to participants. The loan charge itself means the full borrowed amount (not just unpaid tax, but the entire sum) is treated as income. For someone who borrowed £100,000 across multiple years through a scheme, a single tax year’s assessment could trigger a bill of £40,000–£60,000 in tax and National Insurance contributions alone, plus interest accrued since April 2019 and potential penalties.

Landlords are equally exposed. Some have used loan schemes to finance property purchases, treating the borrowed funds as tax-free loans rather than taxable income. HMRC’s updated guidance makes clear this is not a permitted structure.

What makes this urgent: if you have not yet been contacted by HMRC but participated in a scheme, the clock is still running. HMRC can open assessments going back many years if you have not made a full disclosure. The longer you delay, the more interest accrues and the worse the settlement becomes.

Example: Sarah is an IT contractor who participated in an employment trust loan scheme between 2015 and 2019. She “borrowed” £80,000 across four tax years (£20,000 per year) and paid minimal income tax during that period because the scheme promoter told her the loans were tax-free. In reality, her contract income was £120,000 per year. HMRC discovers the arrangement through the scheme promoter’s records. The loan charge applies: all £80,000 is treated as income in 2018–19. Combined with National Insurance, Sarah now owes approximately £35,000 in unpaid tax and NI. Interest from April 2019 to the present adds a further £8,000. A careless penalty of 30% adds another £12,900. Sarah’s total bill: approximately £55,900. Had she settled the loan charge earlier through the Loan Charge Settlement Terms (which offered some penalty mitigation), her cost would have been substantially lower.

Godwin Pinto ACA, ICPA, founder of AccTek, comments: The republication of this guidance tells us HMRC is moving into a more aggressive recovery phase. We’re seeing clients come to us in a state of shock—they genuinely believed the scheme was legitimate because a promoter told them so. The hard truth is that HMRC has now assessed or is assessing thousands of individuals, and the loan charge has proven devastating for those caught. What I’m telling clients now is simple: if you’re uncertain whether you participated in a flagged scheme, don’t wait for HMRC to find you. The sooner you engage with HMRC through a professional adviser, the sooner we can explore settlement options and potentially reduce the final bill. Silence is the worst strategy—interest compounds monthly, penalties apply to unpaid tax, and HMRC has unlimited time to pursue you if your tax return was careless or deliberate. I’ve also noticed that some contractors mistakenly believe recent discussions with their accountant about their past arrangements constitute adequate disclosure. They don’t. HMRC wants a formal disclosure followed by payment or a structured payment plan.

The cost of non-action far outweighs the cost of professional advice. If you participated in any loan scheme or are uncertain about your tax position, contact AccTek today for a free, confidential consultation with a tax specialist. Visit AccTek’s instant quote page to discuss your situation and explore your options—because when it comes to loan charges, early action saves money.

Official guidance

For the latest HMRC guidance on the loan charge, see how to report and account for the disguised remuneration loan charge and HMRC’s guidance on settling your tax affairs. AccTek Ltd is an independent accountancy firm and is not affiliated with HMRC or GOV.UK.

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 14 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.