Hello, medical masterminds! 🩺

As a Chartered Accountant who spends an unhealthy amount of time translating tax legislation into human English, I often notice a fascinating paradox: doctors can recall the most obscure anatomical anomalies under extreme pressure, yet they regularly freeze when handed a simple HMRC tax code coding notice.

And look, I completely get it. You are working back-to-back shifts, managing complex patient cases, and trying to stay hydrated. Checking your tax account is rarely a top priority.

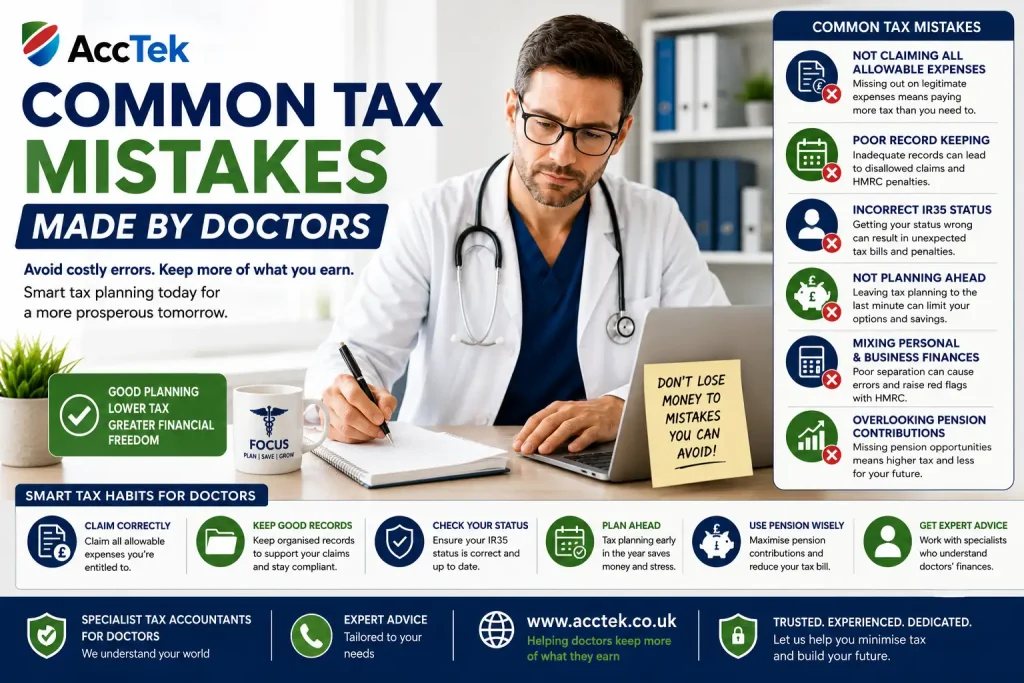

However, mismanaging your tax profile can result in thousands of pounds slipping straight through your fingers. As we navigate the 2026/27 tax year and look toward 2027/28, HMRC is intensifying its scrutiny on high earners and medical practitioners alike. Let’s diagnose the 5 most common tax mistakes doctors make and prescribe the exact financial treatments to fix them.

This is the absolute bane of a junior doctor’s existence. Every year in August, thousands of training doctors pack up their stethoscopes and rotate to a brand-new NHS Trust.

Dr. Maya moves from an NHS Trust in London to one in Surrey. Because of a lag in the legacy payroll system, her old employer issues a final payslip around the same time her new employer processes her first one.

HMRC’s automated systems spot this and panic, assuming Maya has suddenly taken on a secret second full-time job. To protect their tax take, they slap an emergency tax code like BR (Basic Rate, taxing everything at 20%) or D0 (Higher Rate, taxing everything at 40%) on her new payslip, completely stripping away her tax-free Personal Allowance of £12,570. If you earn more than £100k then this mistake could be fatal.

The Fix: Never ignore your payslip. If your tax code says anything other than 1257L (assuming you have a standard allowance) or contains “BR”, “D0”, or “X”, you are paying too much tax. Log into your HMRC Personal Tax Account on GOV.UK immediately to update your current employer details and force an automated correction.

To practice medicine in the UK, you have to pay a small fortune in mandatory professional fees. Surprisingly, an enormous percentage of salaried NHS doctors forget that these are fully tax-deductible!

If you pay for these out of your post-tax salary, you are entitled to a significant tax rebate. For a higher-rate (40%) or additional-rate (45%) taxpayer, this effectively gives you nearly half your money back.

HMRC maintains an officially approved list of professional bodies. If your subscription is on it, it counts. This includes:

The GMC Retention Fee

The BMA Subscription

Medical Indemnity (MDU, MPS, MDDUS)

Royal College Membership Fees

You can check the full list and confirm what qualifies by visiting the official HMRC Doctors’ Expenses Help Sheet (HS231) or a simplified summary of expenses you can claim.

HMRC allows you to claim travel costs, but their definition of business travel is incredibly strict. The absolute golden rule is that expenses must be incurred “wholly and exclusively” for the purpose of your work.

What Triggers Unexpected HMRC Travel Inquiries?

🚗 Claiming normal home-to-base hospital commuting [███████████████] 50%

🗺️ Forgetting to log actual multi-site mileage logs [██████████] 30%

🛑 Confusing "on-call" travel with business trips [██████] 20%

If you travel between different clinical sites, hospitals, or ad-hoc community clinics for locum assignments, you are eligible to claim mileage.

And there is huge news for this tax year: Following recent Treasury announcements, the HMRC approved mileage rate has officially increased to 55p per mile for the first 10,000 miles (up from the frozen 45p rate of previous years). If you are commuting to a single “permanent” place of work, that is normal commuting and completely disallowed. But if you are travelling to temporary assignments, make sure you claim at the new, generous 55p rate!

If you handle private consultations, cosmetic procedures, or write medico-legal reports, you probably operate as a sole trader alongside your NHS role. A classic mistake here is accounting for your income based on when the cash hits your bank account.

In the UK tax framework, standard accounting rules dictate that you must declare your income based on the invoice date, not the payment date.

If you invoice a solicitor £2,000 for an expert witness report in March 2027 (inside the 2026/27 tax year), but they don’t actually pay you until June 2027 (inside the 2027/28 tax year), that £2,000 must still be declared on your 2026/27 tax return. Failing to align your dates correctly can land you with unexpected late-payment penalties from HMRC.

The NHS Pension Scheme is an incredible asset, but its growth calculation mechanics are notoriously volatile. For the 2026/27 tax year, the Pension Annual Allowance sits at £60,000.

Your annual allowance isn’t measured by the physical cash you pay out of your paycheck; it’s calculated based on how much the total value of your future pension benefit has grown over the year, using a complex HMRC multiplier formula.

If you take on significant overtime, secure a major clinical promotion, or stack up high-paying locum shifts, your pension value can spike dramatically. If this growth breaches the £60,000 threshold, you face a severe, unexpected tax surcharge.

| The Tax Mistake | The Financial Symptom | The Accountant’s Prescription |

| Ignoring an emergency tax code | Slashes your monthly net take-home pay by dropping your personal allowance. | Check your payslip monthly for code 1257L. Update HMRC online if it’s wrong. |

| Forgetting GMC/BMA/MDU fees | Leaving hundreds of pounds of legal tax relief unclaimed. | Backdate a claim for up to 4 years using a P87 form or your Self Assessment. |

| Claiming normal hospital commuting | Triggers severe HMRC penalties and audit reviews if picked up. | Only claim mileage for temporary workplaces or multi-site clinical travel. |

| Failing to track total pension growth | Massive, surprise tax bills landing out of nowhere at year-end. | Request an Annual Allowance Statement from NHS Pensions annually. |

Taxes don’t have to be a source of stress. By reviewing your monthly payslips, tracking your business mileage diligently at the new 55p rate, and logging your professional subscriptions, you can keep your tax profile completely clean and optimized.

If your income tracks above the £100,000 mark or you juggle a mix of NHS payroll, private work, and locum shifts, partner with a specialist medical Chartered Accountant. We will handle the compliance diagnostics so you can focus on your patients!

Have you checked your latest payslip to see if your current tax code is set to 1257L, or do you suspect you might be sitting on an emergency code after a recent shift rotation?

Need specialist help with your locum doctor tax?

AccTek’s locum doctor accountant service handles everything from Self Assessment to NHS pension reviews — fixed fees from £19.99/month.

Related reading:

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 14 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.