Hello, medical masterminds! 🩺

As a Chartered Accountant who genuinely enjoys reading 80-page pension manuals (yes, we do exist, and no, we are not okay), I know how much you love dealing with paperwork. Which is to say: you would rather do a double shift in A&E with a broken coffee machine.

But when it comes to the NHS Pension Scheme, tuning out can cost you tens of thousands of pounds. It is widely considered one of the most generous defined-benefit pension schemes in the UK, providing a guaranteed, inflation-linked income for life.

However, for freelance locum GPs and sessional doctors, the pension rules aren’t quite as straightforward as they are for salaried consultants. Between the strict deadlines, the 90% rule, and the dreaded “Annualisation Monster,” it’s easy to get a financial headache.

Let’s break down the NHS Pension rules for the current 2026/27 tax year and looking forward to 2027/28, complete with some vital HMRC tax-planning checkpoints.

Before you write your next invoice, you need to understand the fundamental mechanics of how a locum doctor’s income is pensioned.

You cannot pension your entire invoice amount. HMRC and the NHS Business Services Authority (NHSBSA) dictate that your pensionable income is exactly 90% of your gross fee (excluding any employer contribution elements). The other 10% is legally assumed to cover your business running costs (like indemnity insurance, accounting fees, and stethoscopes).

This is the biggest trap in medical finance. If you operate as a Limited Company, you cannot join or contribute to the NHS Pension Scheme for that work. The NHS Pension Scheme is strictly for individuals (sole traders) or partners. If your contract is Outside IR35 and paid into your corporate business account, the NHS Pension is off the table.

You must record and submit your locum forms (Form A and Form B) within 10 weeks of completing the work. If your forms arrive at Primary Care Support England (PCSE) or your local health board on week 11, they will be flatly rejected, and you will lose the right to pension that income.

How much do you actually pay? The NHS Pension operates on a tiered system. For the current 2026/27 year (effective from 1 April 2026), the thresholds have been automatically indexed by the September 2025 CPI rate of 3.8% to prevent inflation from accidentally pushing you into a higher bracket.

Here is exactly what you will pay based on your annualised pensionable earnings:

| Pensionable Pay Range (From 1 April 2026) | Member Contribution Rate |

| Up to £13,259 | 5.2% |

| £13,260 to £28,854 | 6.5% |

| £28,855 to £35,155 | 8.3% |

| £35,156 to £52,778 | 9.8% |

| £52,779 to £67,668 | 10.7% |

| £67,669 and above | 12.5% |

Note: On top of your contribution, the NHS contributes 23.7% (with 14.38% collected from the surgery/trust and the rest covered centrally by the government). That is essentially free retirement money!

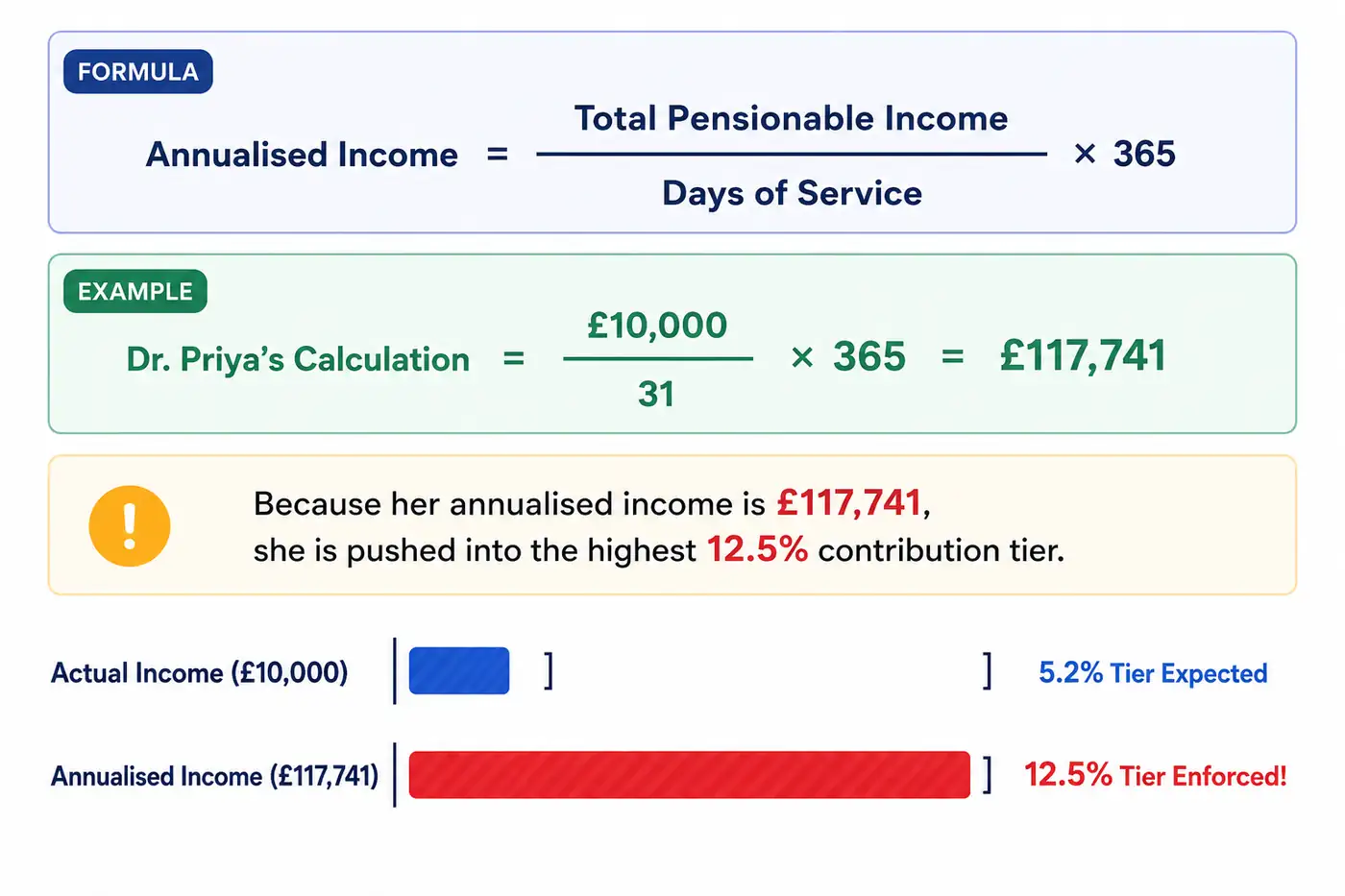

If you work continuously throughout the year as a salaried GP or consultant, your pension tier is simple. But if you are solely a freelance locum doctor who works irregularly, you fall victim to annualisation.

The NHS Pension Scheme calculates your contribution tier based on what you would have earned if you worked at that exact pace for a full 365 days.

Dr. Priya decides to take a break from medicine to travel. However, she spends the entire month of August 2026 smashing out locum shifts, earning a total pensionable income of £10,000 across 31 days. She doesn’t work any other pensionable shifts for the rest of the year.

Instead of looking at her actual income (£10,000, which would put her in the 5.2% tier), the annualisation formula scales it up:

The Accountant’s Remedy: If you are going to pension your locum work, try to avoid long, empty gaps between pensioned days within the financial year, or map out your shifts strategically using the official annualisation calculators provided by the NHSBSA.

Because you pay pension contributions out of your earnings, HMRC gives you generous tax relief on that money. For the 2026/27 and 2027/28 tax years, the Pension Annual Allowance sits at £60,000.

As a self-employed locum doctor, you do not get automatic tax relief through an employer’s payroll system. Instead, you must claim it manually.

When your accountant prepares your Self Assessment tax return at the end of the year, your total pensionable net contributions must be declared. This expands your basic rate tax bands, effectively giving you back 40% or 45% tax relief depending on your earnings bracket.

HMRC Checkpoint: Always make sure your total pension growth (including your NHS added years or AVCs) doesn’t breach the £60,000 Annual Allowance, especially if your total Adjusted Net Income climbs over £260,000, where the allowance begins to taper down. You can check the live limits directly via the HMRC Pension Tax Relief Guidance on GOV.UK.

To make sure your retirement pot is growing smoothly without triggering an HMRC audit, follow this quick diagnostic checklist:

Calculate the 90% split: Ensure your Locum Form A only records 90% of your raw fees as pensionable pay.

Watch the calendar: Submit your Locum Form B and your payments to PCSE Online within 10 weeks of the shift ending.

Check your business structure: Remember, if you are invoicing under a Limited Company name, you cannot submit those earnings into the NHS Pension. Consider IR35 implications.

Track your annualisation: Keep a calendar log of every day you worked a pensionable shift to protect yourself against sudden tier jumps.

The NHS pension is incredibly lucrative, but it requires active management. If you feel your paperwork piling up or you aren’t sure how your locum income interacts with an existing NHS contract, drop a line to a specialist medical accountant. We will get your financial health back to a perfect 120/80! And donât forget â claiming your allowable locum expenses reduces your taxable income, which in turn can help keep you below the annual allowance threshold. Failing to track your allowance is one of the most expensive errors we see â read our guide to common tax mistakes made by doctors to avoid it.

Need specialist help with your locum doctor tax?

AccTek’s specialist locum doctor accountant service handles everything from Self Assessment to NHS pension reviews — fixed fees from £19.99/month.

Related reading:

Disclaimer: This blog post is for educational and entertainment purposes only and does not constitute formal financial, pension, or tax advice. Pension rules are subject to individual circumstances and regional differences (England/Wales vs. Scotland/Northern Ireland). Always consult a qualified Chartered Accountant or an independent financial advisor before making major pension decisions.

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 14 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.