Hello again, medical movers and shakers! 🩺

As a Chartered Accountant who specializes in keeping doctors on the right side of the taxman, there is one acronym that I see striking absolute dread into the hearts of locum clinicians: IR35.

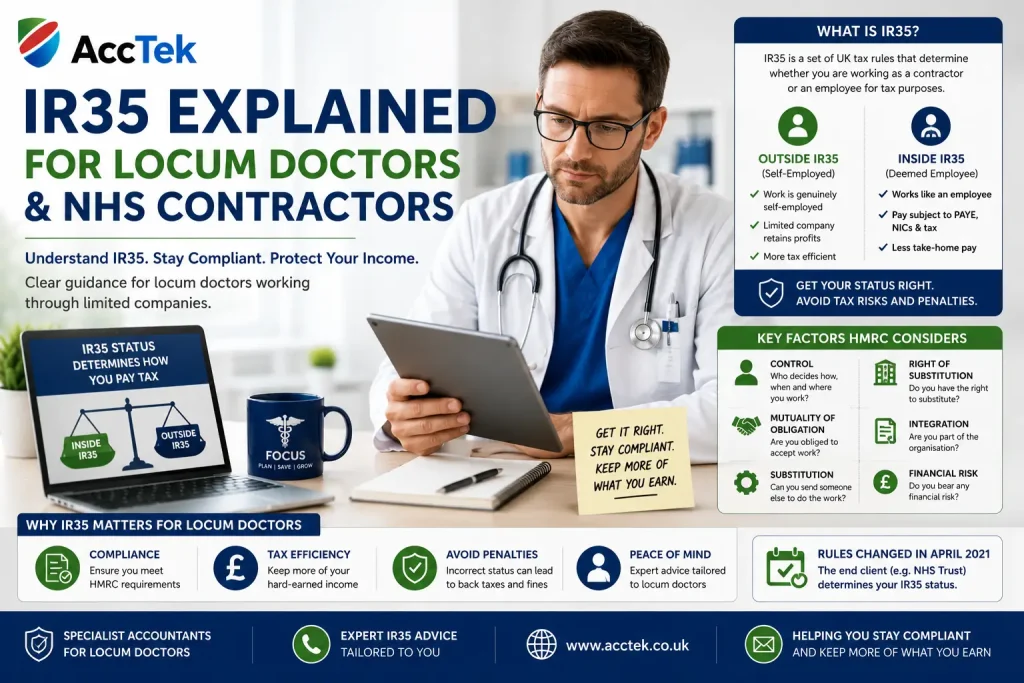

It sounds like a rare strain of flu or a top-secret military drone, but it’s actually HMRC’s framework for off-payroll working rules. If you are a locum doctor operating via an agency, a staff bank, or your own Limited Company (often called a Personal Service Company or PSC), IR35 dictates exactly how your hard-earned cash is taxed.

As we navigate the current 2026/27 tax year and look ahead to 2027/28, the landscape is sharper than ever—especially with brand-new HMRC regulations targeting umbrella companies. Let’s break down the rules, look at a real-world scenario, and inject some clarity into your tax planning.

In a nutshell, IR35 is designed to stop what HMRC calls “disguised employment.”

Imagine an NHS hospital that wants to hire a full-time A&E registrar. Instead of hiring them as an employee, they hire the doctor through the doctor’s own micro-company. The doctor does the exact same job as the salaried staff but pays significantly less tax by taking dividends instead of a salary, while the NHS trust avoids paying employer National Insurance.

HMRC created IR35 to say: “If it looks like an employee, acts like an employee, and works like an employee, it should be taxed like an employee.”

To figure out if a locum shift falls “Inside” or “Outside” IR35, HMRC and the courts look at three main pillars:

Control: Does the hospital dictate exactly how, when, and where you work? (For clinicians, the answer is almost always yes).

Substitution: Can you send a qualified friend to cover your shift if you fancy going to a concert instead? If the answer is no (because the hospital requires you specifically), you fail the substitution test.

Mutuality of Obligation (MOO): Is the hospital obligated to offer you shifts, and are you obligated to accept them?

For the 2026/27 tax year, the rules on who decides your status remain firmly fixed. Because NHS trusts and large private hospitals are public or medium/large organizations, the responsibility for deciding your IR35 status sits with them, not you. They will issue a Status Determination Statement (SDS) for your role.

Here is how the two statuses stack up for a locum doctor:

| Feature | Inside IR35 | Outside IR35 |

| Tax Treatment | Taxed like a standard employee via PAYE. | Paid Gross into your Limited Company. |

| Deductions | Income Tax and National Insurance are taken before you see the money. | You pay Corporation Tax and extract money via dividends. |

| Where is it found? | Virtually all NHS staff banks and standard agency locum rotas. | Highly specialized consultancy, ad-hoc private clinics, or niche training. |

| Business Expenses | Very restricted. No travel or mileage to a regular hospital. | Fully allowable business expenses (equipment, accounting fees, mileage). |

If you are inside IR35, you likely use an Umbrella Company to process your payroll.

Take note: Following legislation rolled out on 6 April 2026, HMRC introduced strict joint and several liability rules for the supply chain. If an umbrella company uses non-compliant, dodgy loan schemes to artificially boost your take-home pay, HMRC can now legally pursue the recruitment agency or end-client for the unpaid tax.

The Accountant’s Prescription: This means reputable agencies are vetting umbrella companies harder than ever. Avoid any company offering “90% take-home pay”—it is highly illegal. Stick strictly to FCSA-approved payroll providers. You can read the official guidelines on Understanding Off-Payroll Working on GOV.UK.

Let’s look at Dr. Chloe, an experienced locum medical registrar. She is looking at two different contracts for the upcoming months:

Chloe takes a 3-month block of weekend shifts at a local NHS trust through an agency. The trust issues an SDS stating the role is Inside IR35.

The Reality: She is put on the payroll. Income Tax and employee National Insurance are sliced off her top-line rate before it hits her bank account. She doesn’t need to use her Limited Company for this at all.

Chloe is hired by a small private firm to design and occasionally execute a bespoke corporate health screening program for an executive client. They agree she can send another qualified doctor if she is unavailable, and she uses her own specialized mobile diagnostic kit.

The Reality: Because it’s a small private client and the working conditions have genuine autonomy, it is deemed Outside IR35. She invoices them via her Limited Company, receives the money gross, and works with her accountant to pay herself tax-efficiently using the 2026/27 dividend allowances.

Because “Inside IR35” forces you onto PAYE, your net take-home pay takes a significant hit compared to a genuine “Outside IR35” corporate structure.

[Estimated Take-Home Distribution per £1,000 Gross Revenue]

Inside IR35 (PAYE/Umbrella) [████████████░░░░░░░░] ~60% Take-Home (Tax/NI/Fees deducted)

Outside IR35 (Ltd Company) [████████████████░░░░] ~80% Take-Home (Optimised via Dividends)

(Note: This is an illustrative estimate based on a higher-rate 40% taxpayer bracket for 2026/27, factoring in standard corporate and personal distributions)

If you earn more than £100k in a tax year than the tax difference is severe. No matter which structure you choose you can always claim certain allowable expenses.

If you are offered a private contract or a unique role and want to ensure you aren’t accidentally walking into an HMRC inquiry, you can use the government’s official tool.

HMRC provides the Check Employment Status for Tax (CEST) tool. While it has faced criticism from accountants for being biased toward employment, HMRC explicitly states they will stand by the result provided the information inputted is entirely accurate and reflective of your actual day-to-day working practices.

You can test your contract directly using the HMRC CEST Tool on GOV.UK.

For the vast majority of locum doctors working on standard hospital rotas, Inside IR35 is an inescapable reality of modern medical compliance. Instead of fighting the designation, focus your energy on ensuring your umbrella provider is fully compliant, maximizing your legitimate out-of-pocket allowable expenses on your Self Assessment, and ensuring your pension contributions are structured properly to lower your overall tax bracket.

If you have a mix of NHS bank work and private income, sitting down with a qualified Chartered Accountant to map out your corporate structure for 2026/27 and 2027/28 will prevent any unexpected, painful diagnostic errors from HMRC!

Need specialist help with your locum doctor tax?

AccTek’s specialist locum doctor accountant service handles everything from Self Assessment to NHS pension reviews — fixed fees from £19.99/month.

Related reading:

Disclaimer: This blog post is designed for educational and entertainment purposes. IR35 status depends entirely on the specific wording of your contract and the reality of your working arrangements. Always seek professional advice from a specialist medical accountant before altering your business or tax structure.

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 7 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.