Congratulations! Cracking the £100,000 salary mark is a massive milestone in a medical career. Whether it’s from climbing the NHS consultant ladder, picking up high-yield locum shifts, or expanding your private practice, you’ve earned every single penny through years of sacrifice, exams, and night shifts.

But as a qualified Chartered Accountant, it is my duty to deliver some bittersweet news. In the UK tax system, crossing the £100k threshold triggers an invisible, financially painful phenomenon known as the 60% Tax Trap.

Don’t worry, though. Grab your stethoscope and a coffee—we are going to diagnose exactly how this trap works and write a prescription to help you legally minimize your tax bill for the current 2026/27 tax year and looking forward to 2027/28.

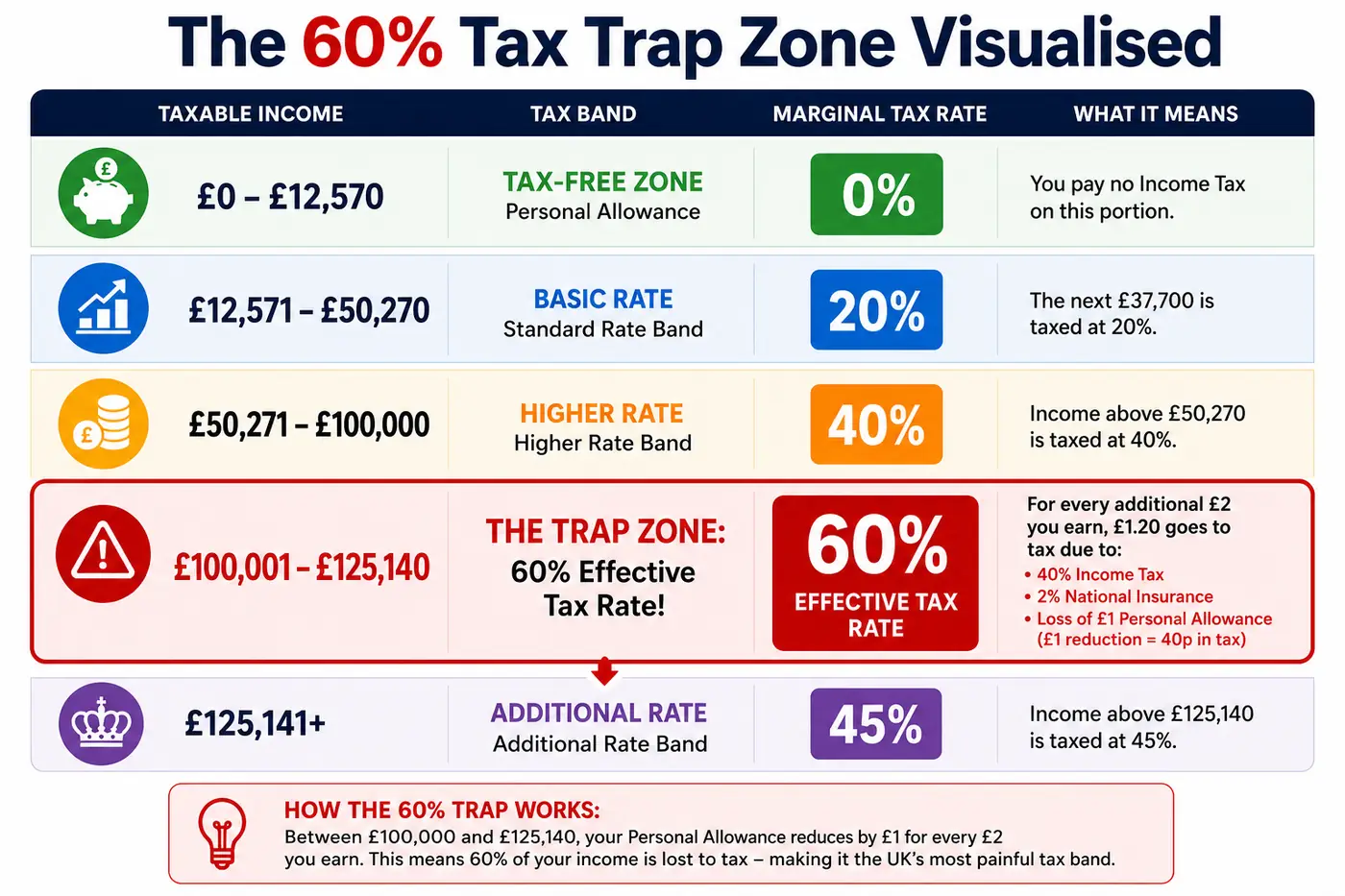

Most people assume that once you cross £50,270, you stay in the 40% “Higher Rate” tax band until you hit the 45% Additional Rate at £125,140. Unfortunately, the reality is much more aggressive.

According to HMRC Personal Allowance Guidelines, your standard Personal Allowance of £12,570 is reduced by £1 for every £2 that your “Adjusted Net Income” goes over £100,000.

Dr. Alex earns £110,000 as an NHS Consultant.

On that extra £10,000, Alex pays the standard 40% higher rate tax (£4,000).

Because of the clawback rule, Alex also loses £5,000 of their tax-free Personal Allowance.

That lost £5,000 allowance is pushed into the 40% bracket, creating an additional £2,000 tax bill.

Total tax on that £10,000 slice of income? £6,000. That is a staggering 60% effective tax rate, and it doesn’t even include National Insurance contributions!

To keep your bearings, here is exactly how the land lies for the current 2026/27 tax year. (Note: If you practice in Scotland, your thresholds and rates are slightly higher, top-ending at a 48% top rate).

| Tax Band | Taxable Income Range | Income Tax Rate | The Reality for Earmarked Income |

| Personal Allowance | Up to £12,570 | 0% | Completely tax-free code. |

| Basic Rate | £12,571 to £50,270 | 20% | Standard rate. |

| Higher Rate | £50,271 to £100,000 | 40% | Where most senior doctors live. |

| The “Trap” Window | £100,001 to £125,140 | 40% (+ 20% Allowance Loss) | The 60% effective tax zone. |

| Additional Rate | Over £125,140 | 45% | Personal Allowance is officially £0 here. |

The secret to beating the trap is reducing your Adjusted Net Income back down to £100,000. HMRC calculates your adjusted net income by taking your total taxable income and subtracting things like personal pension contributions and gift aid donations.

Pensions remain the most potent tool in a doctor’s financial kit. For the 2026/27 tax year, the standard Pension Annual Allowance is £60,000.

If you earn £115,000 and contribute £15,000 (gross) into a regular Private Pension or a Self-Invested Personal Pension (SIPP), your Adjusted Net Income drops precisely to £100,000.

The Result: You completely eliminate the 60% tax hit on that £15,000. Instead of giving £9,000 to HMRC, you keep 100% of it working for you inside your retirement nest egg.

Warning on Defined Benefit (NHS) Schemes: The NHS Pension Scheme is fantastic, but it calculates “contributions” based on the growth of your benefits, not just the cash you pay in. If you have significant private income on top of a senior NHS role, always check your Annual Allowance limits via HMRC Pension Tax Relief Guidance to avoid an unexpected annual allowance tax charge.

If you regularly donate to medical research, local hospices, or international aid charities, ensure you do it under Gift Aid.

When you give £800 to charity, the charity claims an extra £200 from the government (making it a £1,000 gross donation). More importantly for you, that £1,000 gross donation lowers your Adjusted Net Income by £1,000, expanding your tax-free Personal Allowance boundary.

Are you pulling in an extra £20,000–£40,000 a year purely from private clinical work, cosmetic clinics, or expert witness reports? If you operate as a sole trader, that money is piled directly onto your NHS salary, pushing you deep into the 60% trap or the 45% additional rate band.

By setting up a Limited Company for your private work:

The company owns the income and pays Corporation Tax on profits.

You can choose when and how to pay yourself (via dividends or salary).

You can deliberately leave profits inside the company to invest, or pay them out in a future tax year when your NHS income might be lower (e.g., taking a sabbatical or working less sessions).

Note: Be aware that dividend tax rates outside an ISA for 2026/27 sit at 35.75% for higher-rate taxpayers, so corporate planning must be carefully calculated.

To make sure your financial health is as robust as your clinical practice, run through this quick checklist before the end of the tax year:

Calculate your projected earnings: Include basic NHS pay, CEAs (Clinical Excellence Awards), overtime, and private work.

Log your expenses: If you do locum work, ensure you are claiming all allowable expenses including professional fees (GMC, BMA, MDU) and business mileage (which jumped to a generous 55p per mile for 2026/27!).

Review your pension input: Check your latest NHS Pension savings statement to see how much of your £60,000 allowance remains.

Keep a digital paper trail: Use scanning apps to preserve evidence of every business expense or charitable donation.

Taking a preventative approach to your tax planning will save you thousands of pounds. If your situation involves complex NHS pension calculations or layered private income streams, seeking a specialist medical accountant is always your best next move. If you work through an agency or your own company, your IR35 status also affects how your income is taxed and whether you can use these strategies. And if youâre considering incorporation, our guide on whether locum doctors should use a limited company covers the tax implications in detail. Keep up the life-saving work, and let’s keep your hard-earned money where it belongs!

Need specialist help with your locum doctor tax?

AccTek’s locum doctor accountant who specialises in high-earning NHS professionals service handles everything from Self Assessment to NHS pension reviews — fixed fees from £19.99/month.

Related reading:

Disclaimer: This article is for educational purposes and does not constitute formal financial or tax advice. Tax laws can be complex and are subject to change. Always consult a Chartered Accountant or independent financial advisor specializing in medical professionals before making major financial decisions.

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 14 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.