Ah, the age-old medical dilemma. Stethoscope or corporate seal? Scalpel or spreadsheets?

If you are working as a locum doctor in the UK, choosing how to structure your business is one of the biggest financial decisions you’ll make. Get it right, and you are smoothly sailing through tax season. Get it wrong, and you might feel like you’ve accidentally walked into a fiscal emergency room.

With frozen tax bands and evolving rules hitting hard in the 2026/27 tax year, the question remains: Should locum doctors use a limited company? Let’s unpack the pros, cons, NHS pension traps, and the infamous IR35 rules to find your perfect financial prescription.

Before looking at the math, let’s look at the two primary structures available to a locum doctor running a limited company or operating as a self-employed individual.

Sole Trader: You are the business. It’s simple to set up, requires less paperwork, but leaves you personally liable for business debts. Your earnings are taxed directly via Self Assessment.

Limited Company: The company is a separate legal entity. It owns the money, bills the hospitals or clinics, and pays Corporation Tax. You then pay yourself through a smart combination of a low salary and dividends.

| Pros | Cons |

| Tax Flexibility: You control when and how much you pay yourself. | Higher Admin: Monthly payroll, annual accounts, and Companies House filings. |

| Limited Liability: Your personal assets (like your home) are protected. | Accountant Fees: You’ll need a qualified accountant to keep you compliant. |

| Corporate Perks: Ability to claim a wider range of business-justified expenses. | IR35 Risk: If caught by IR35, the tax advantages can disappear instantly. |

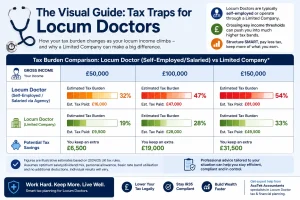

Why do people love limited companies? In two words: Tax Efficiency.

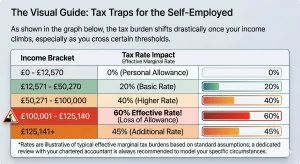

As a sole trader, every penny you earn above the frozen Personal Allowance of £12,570 is subject to Income Tax (20%, 40%, or 45%) and National Insurance contributions.

Through a limited company, your company pays Corporation Tax on profits (ranging from 19% to 25% depending on profit levels). You then extract the cash. Dividends do not attract National Insurance, and dividend tax rates are lower than standard income tax rates.

As shown in the graph below, the tax burden shifts drastically once your income climbs, especially as you cross certain thresholds.

We cannot talk about the best structure for locum doctors without addressing the elephant in the hospital ward: IR35.

According to HMRC’s off-payroll working rules, if your locum contract is deemed “Inside IR35”, HMRC views you as an employee for tax purposes.

⚠️ The Inside IR35 Rule: If your shift is Inside IR35, operating through a limited company is virtually pointless. You will be taxed at source via PAYE (often through an umbrella company), eliminating any corporate tax savings while leaving you with all the limited company paperwork.

Most direct NHS locum shifts booked through banks are inside IR35. However, private work, certain GP locum roles, and specialized consultancy work may still comfortably sit Outside IR35, where a limited company shines.

The NHS Pension Scheme is one of the finest golden handcuffs in the country. For the 2026/27 tax year, employee contribution tiers range from 5.2% up to 12.5% based on your actual annual pensionable pay.

Here is the catch: You cannot pension your income through the NHS Pension Scheme if it is paid into a Limited Company.

If you value building up your NHS Pension, working as a sole trader (using Form A and Form B for GP locums) or via PAYE is mandatory.

If you have already maxed out your lifetime allowance or prefer to build a private pension pot, a limited company allows you to make highly tax-efficient corporate pension contributions directly from the company bank account, lowering your Corporation Tax.

If your work is Outside IR35, when does the scale tip in favor of a limited company?

Historically, the tipping point was around £50,000. In 2026, due to rising compliance costs and Corporation Tax tweaks, it is generally worth incorporating if your net profit consistently exceeds £70,000 to £80,000, and you do not need to draw out all your profits to live on.

If you earn £100,000+, a limited company becomes an incredibly powerful shield.

For every £2 you earn over £100,000, you lose £1 of your tax-free Personal Allowance. This creates a brutal 60% effective tax rate on income between £100,000 and £125,140.

The Limited Company Solution: If your company bills £130,000 in a year, you can choose to draw a salary and dividend combo total of £99,000—keeping your personal income safely below the cliff edge. The remaining £31,000 (minus Corporation Tax) can sit safely inside your company bank account to be drawn in a later year, used for business expenses, or invested into a private pension.

There is no one-size-fits-all “best structure for locum doctors”. If your shifts are inside IR35 and you want to build an NHS pension, a limited company will only cause you headaches. But if you have significant income outside IR35, earn over £100,000, or want to control your tax timing, incorporating could save you thousands.

Every doctor’s financial anatomy is unique — and doctors who incorporate without specialist advice often make avoidable errors. Our guide to common tax mistakes made by doctors covers the pitfalls to watch for. Book a consultation to review whether a limited company is right for your situation. Let’s run a full financial diagnostic on your earnings and build a strategy that keeps more money in your pocket.

Need specialist help with your locum doctor tax?

AccTek’s AccTek’s locum doctor accounting service service handles everything from Self Assessment to NHS pension reviews — fixed fees from £19.99/month.

Related reading:

Godwin Pinto ACA is a chartered accountant and founder of AccTek with 20+ years of experience accounting and tax for contractors, startup and SME .

Last updated: 14 June 2026

AccTek is a member firm of the Institute of Certified Practising Accountants (ICPA). Our accountants have a wide range of qualifications and accreditations from trusted professional bodies such as the AAT, ICPA, and ACCA.